- City Fajr Shuruq Duhr Asr Magrib Isha

- Dubai 04:18 05:40 12:28 15:52 19:10 20:33

A slowing rate of decline across all sectors of the Dubai real estate market suggests increasing stability and the expectation of the market ‘bottoming out’ before the end of 2017, according to leading international real estate consultancy, Cluttons.

Cluttons’ Dubai Spring 2017 Property Market Outlook reports that despite the persistence of market corrections in Q1 2017, average residential prices have moderated by 0.9% with the annual rate of decline slowing from -8.8% at the close of 2016 to -7.8% at the end of March.

Increasing supply, changing demand for executive positions in the employment market and increasing rent moderation are all expected to continue to impact the residential market during 2017. In the Dubai office market, the planned introduction of VAT on January 1st 2018 is already causing a nervousness amongst existing tenants, the Cluttons report finds.

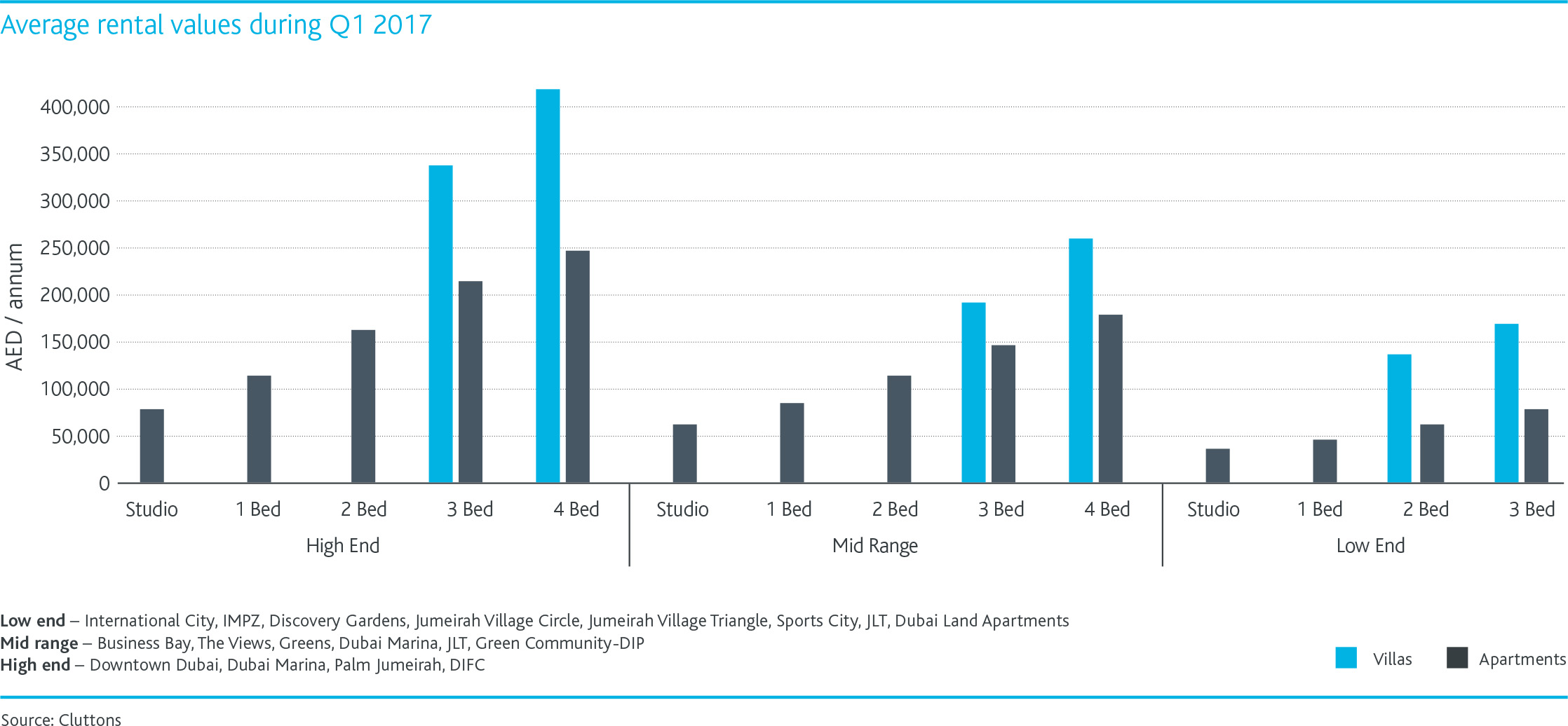

Residential Market

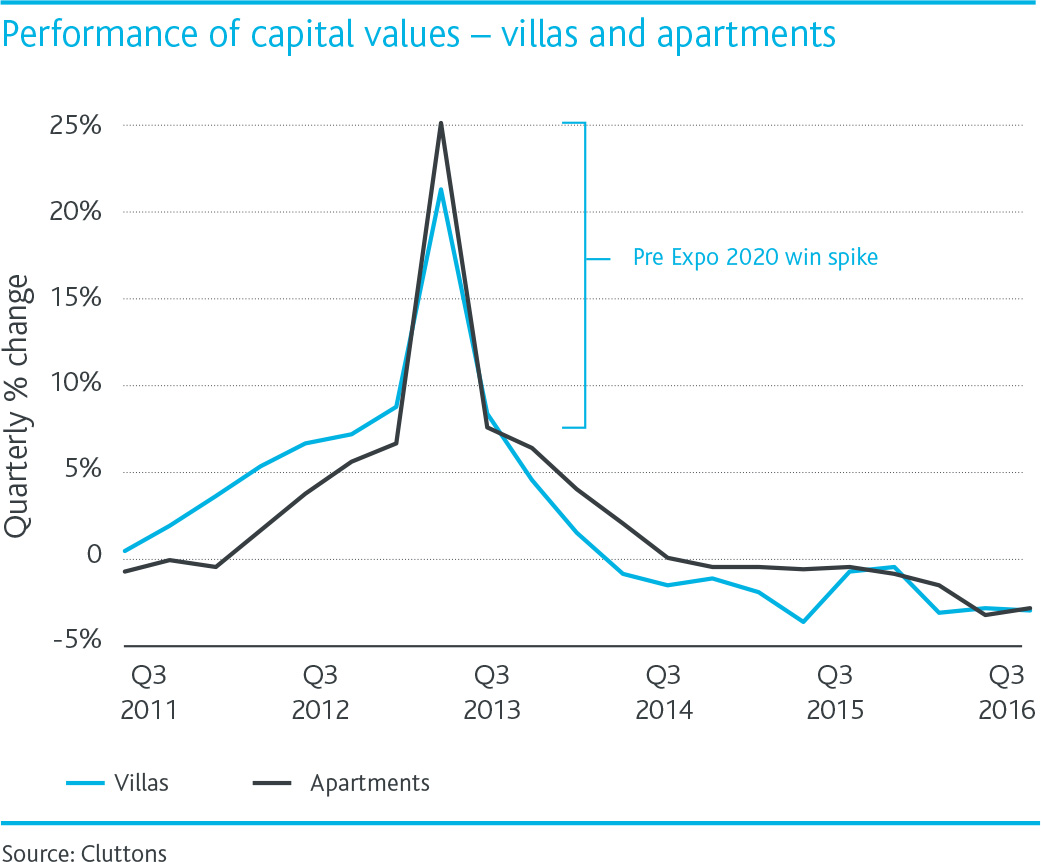

As referenced, values across Dubai’s freehold residential areas slid by 8.8% in 2016, largely in line with Cluttons’ original forecast for the year of -10%. This signals the market’s weakest annual performance in five years, and sits 28.7% below the Q3 2008 market peak.

Commenting on the residential market, Faisal Durrani, Head of Research at Cluttons said, “While local economic drivers may appear robust, regional and global economic uncertainty has undoubtedly curtailed domestic growth.

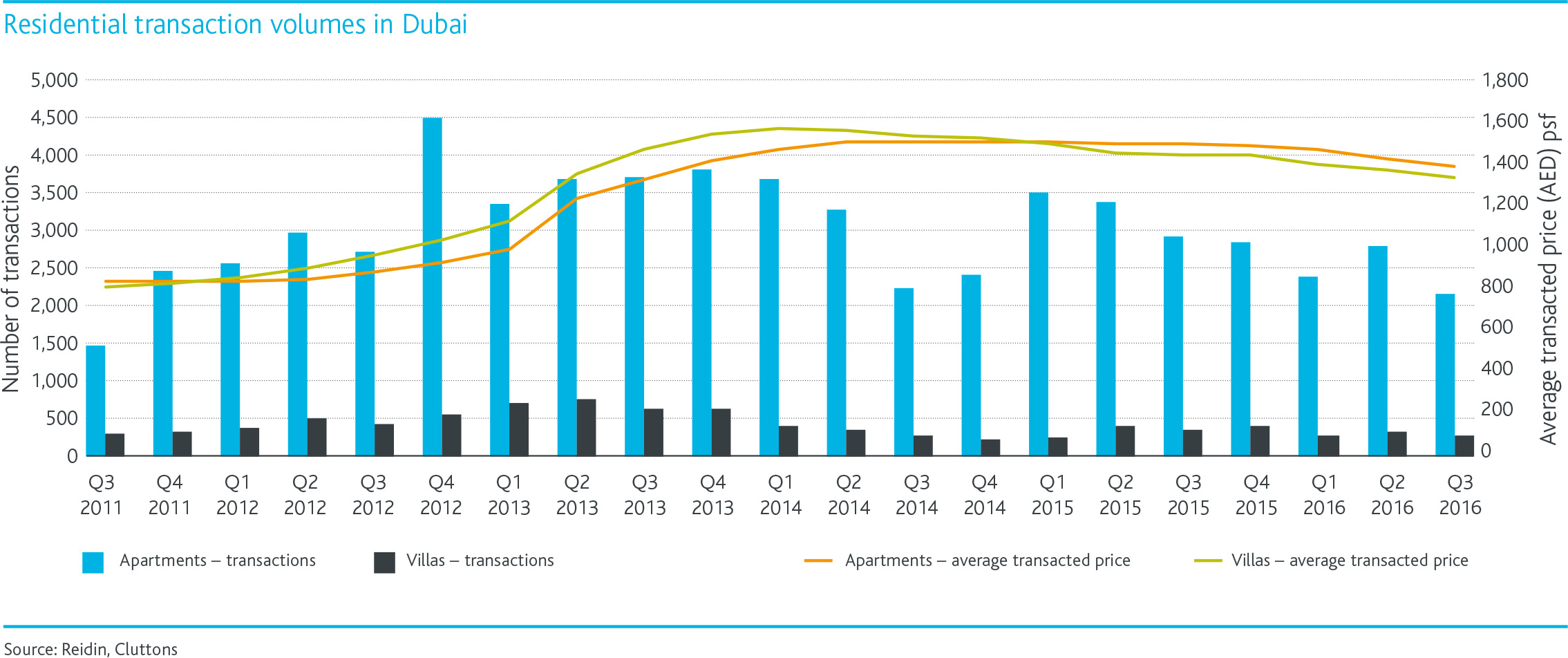

Despite this, the off-plan residential sales market has remained resilient and in fact accounted for 53% of all deals in 2016, suggesting that investor confidence remains strong.

Clearly this has been aided by some exceptionally favourable payment plans that stretch beyond handover, negating the need for financing from the get-go, in addition to attractive gross rental yields.”

“Despite the emerging focus on the residential investment market, tenant demand remains mute and has undoubtedly eased over the last 12 months.

This contributed to the 9.9% drop in average rents last year. The rate of creation of senior level executive positions has fallen and this is reflected in the lower level of enquiries and budgets we are recording.

The redundancy programmes in the city’s finance & banking sector and oil & gas sector have all but run their course, but the weak global outlook is putting other key sectors under pressure, including the hospitality and aviation sectors, both of which are long standing and historic cornerstones of economic growth. The rapid and sudden strengthening of the US dollar over the last 9 months has added to the challenges faced by the property market.”

Part of this overall market weakness lies at the top. 12 of the 32 submarkets monitored by Cluttons registered price declines during Q1, with the Burj Khalifa tower (-6.9%) leading the price falls. Over the last 12-months, the Burj Khalifa has registered a 25% correction in values, making it the weakest performer across the city.

Hattan Villas at The Lakes (-13.5%), Hattan Villas at Arabian Ranches (-12.6%), villas on the Palm Jumeirah (-12.3%) and apartments on the Palm Jumeirah (-11%) rounded off the list of the five weakest performing markets over the last 12 months, the Cluttons report finds.

Murray Strang, Head of Cluttons Dubai, noted, “Aside from the ultra-luxury of the Burj Khalifa tower, the lifestyle and destination living appeal of Downtown Dubai has in a way insulated the market’s performance from the fall out of global geopolitical events. Bahwan Tower for example, which is located within the Burj Khalifa community, launched in November 2016 and is a prime example of sustained demand, as a strong sales performance continues ahead of a Q4 2017 completion”.

Cluttons latest report also finds that a limited number of vacant plots remain within the Mohammed Bin Rashid loop, suggesting that the resilience in values is likely to persist as new opportunities to purchase in this submarket start to diminish. In fact, there was a 47% drop in the number of units launched in Downtown Dubai during 2016, with just 1,431 new homes released, compared to 2,104 unit launches in 2015.

Strang added, “While the short-term prospects appear relatively subdued, our view is that the rental market’s fortunes remain tied to the looming 2020 World Expo. At this stage, the mega event is one of the primary upside risks to our outlook. We know from experience that the lag between the take up of office space and the subsequent impact on the residential rental market is usually six to nine months. Construction contracts worth AED 11 billion, linked to the Expo, are expected to be announced throughout the course of 2017, driving up the rate of job creation and tenant demand in its wake, but this is not expected for another two to three quarters at least.”

Durrani highlighted, “However before the ‘Expo effect’ ripples through the market, we expect that rents will continue moderating during 2017, with an average decline of 5% to 7% likely over the course of the next six months.

A key factor in the rental market’s fortunes will be its ability to absorb the strengthening stream of buy-to-let homes, which has already upset the delicate supply-demand equation.

Any impact on the sales market will likely follow, however for now we anticipate capital values will moderate by a further 5% on average before there is the potential for a more stable picture to emerge towards the end of 2017.”

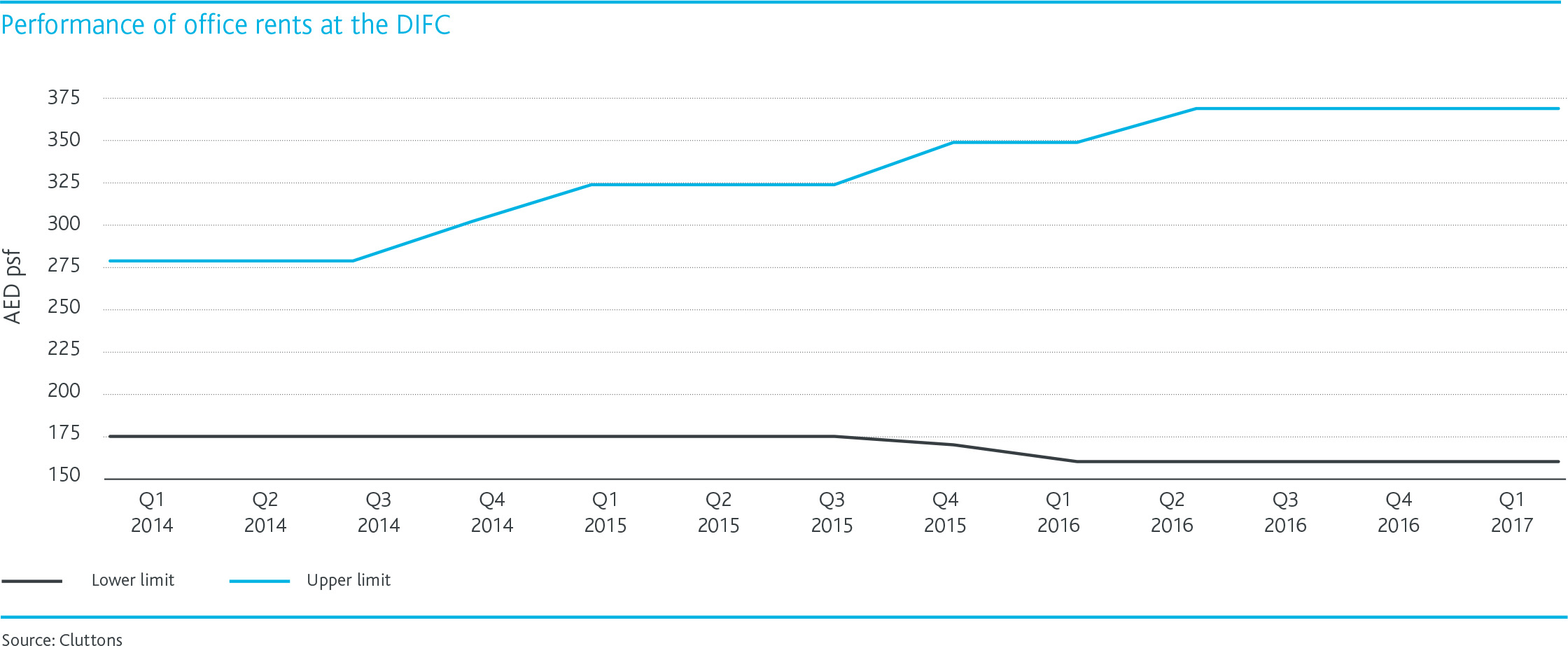

Office Market

Cluttons’ report stresses the combination of VAT uncertainty and market pressures being faced by the city’s office market, which has remained relatively unscathed by the deteriorating global economic conditions.

The Cluttons Dubai Spring 2017 Property Market Outlook reports that rents across most of the 24 submarkets monitored remained relatively steady throughout 2016, following strong growth in the preceding 12 to 18 months. However, global economic anxiety and a subsequent scaling back or delaying of short term expansion projects, particularly amongst international corporate occupiers, has begun to impact on the resilience of rents.

Strang added, “Furthermore, uncertainty stemming from the proposed introduction of a Value-Added-Tax (VAT) is causing some nervousness in the market.

For many international occupiers, it is likely that this is something they will be able to take in their stride, given that they are used to taxation regimes in their own home markets; however, for international occupiers from the UK, or Europe, the prospect of a 5% tax on rental payments, combined with a rise in operational costs fuelled by the strength of the US dollar, may dampen take up activity in the short to medium term.

It remains unclear at this stage whether firms operating within free-zones will be exempt from any potential VAT charges, however it is our expectation that any new tax will be applied across the board to limit an exponential rise in requirements for free-zone office space.”

In general, however, Cluttons claims the overall slowdown in activity levels has resulted in headline rents dipping back marginally.

Strang concluded, “High demand areas such as TECOM’s Internet City and Media City, in addition to core locations within the DIFC remain well let, with stable rents. A limited supply pipeline in both markets is clearly supporting the stability in rents. Equally, demand from occupiers to secure a presence in these key areas is reflected in the fact that the DIFC’s new eight storey Gate Village 11 Building, The Exchange, has been reportedly pre-leased, with completion not expected until late 2017, or early 2018”.

![]() Follow Emirates 24|7 on Google News.

Follow Emirates 24|7 on Google News.