- City Fajr Shuruq Duhr Asr Magrib Isha

- Dubai 04:20 05:42 12:28 15:53 19:08 20:30

Steen Jakobsen, Chief Economist & CIO / Saxo Bank

It's a great irony that we have a Brexit vote coming up, as I would argue that UK never actually really joined the European Union. Being a child of the 1970s and 1980s, I remember vividly how Ms T - T as in Thatcher - fought the EU over everything and somehow managed to make EU comply with her version of the union... at least financially.

It's an even greater irony that prime minster David Cameron has already secured the UK ability's to not be part of a Europe moving forward as his deal with Brussels in March de facto creates a two-tier Europe with one set of rules for the UK and one for the rest of Europe.

Irrespective of the outcome on June 23, this could create a potential mini-crisis in Europe as it's very easy to imagine countries like Hungary, Poland and maybe even Finland wishing to secure deals that match the concessions given the UK.

Europe loses if the UK stays due to this two-tier precedent (breaking the greater union down into smaller ones will ultimately break the "unions") and of course if UK does leave, both the political and the practical costs seems insurmountable - especially as the refugee crisis still very much needs to be dealt with.

I also find it almost hysterical that chancellor Osborne, who can't predict his budget deficit for the next six months, can tell me down to the penny how much each family in the UK will lose by 2030 if they vote for a Brexit (£4,300, apparently).

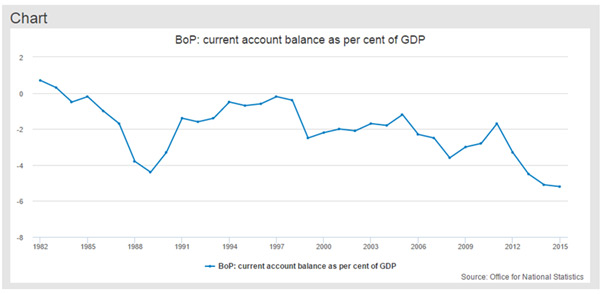

The scare-mongering is crazy, especially for a simple economist like me as the future of the UK really lies in how the UK deals with its chronic double deficit... the country's current account was last positive in 1982. That's 34 years ago!

So to answer the question on every FX trader's mind - where is the GBP headed? - the answer the same with our without a Brexit. Ultimately, the pound will head down or sideways. As long as you spend more than earn, depend on foreign funding, and have an economy whose two growth drivers are is banking and real estate - two sectors with zero productivity and (at best!) uncertain futures in terms of new jobs relative to the recent past - you are doomed to repeat recent history.

Recent history, of course,shows us that London is willing to engineer GBP lower in times of crisis, and a crisis is indeed stalking the UK economy. A more sceptical analyst could even argue that the Brexit is an excellent "hiding place", or excuse, for the coming recession-like economy created by the above fundamentals.

The response to such a situation, of course, has traditionally been a lower GBP.

The Brexit is an abstraction that occludes the real change needed in the UK. It's also an excuse employed to avoid dealing with the more fundamental, structural issue of a society that is moving towards being almost 100% service based.

The UK's basic research and production has been transferred overseas and more importantly, the country's ability to remain a port of call for overseas investors is becoming less and less attractive as non-domicile tax status is changed. Another big game changer following the release of Panama papers is Cameron's call for a public registry for foreign real estate owners.

This is only fair and good as it increases transparency, but it also de facto reduces the "attractiveness" of the UK. I would argue that changed tax rules and hence incentives are far more important than the UK's EU status, as London is already free to apply its own rules.

I am in no way reducing the importance of the vote, but it has very little to do with the future of the UK economy and a lot to do with the role of the UK in Europe.

Let me underline that I don't see any scenario wherein the UK benefits by leaving - not at all, in fact, but this does not mean I am willing to accept the misinformation coming from the "Stay" campaign. The fact is, no one knows what happens next. We do know the "noise" (read: volatility) will increase, but we don't know how the world would look with or without a Brexit.

Maybe it's time to broaden the implications of a Brexit towards the bigger and more important questions: How do we get a mandate for change embedded in both the UK and the EU?

Both entities need to take a close and realistic look at their respective (albeit linked) futures, and to examine their structural design and incentives programmes. At this point, "more of the same" will produce a bleak future.

The most important question of all remains how we deal with the humanitarian crisis posed by the mass arrival refugees in a time of recession risk. How we act here will define both Europe and the UK in the future far more than whether the UK decides to leave a club where it is already free to "behave" as it sees fit.

![]() Follow Emirates 24|7 on Google News.

Follow Emirates 24|7 on Google News.