- City Fajr Shuruq Duhr Asr Magrib Isha

- Dubai 04:18 05:40 12:28 15:52 19:10 20:33

After a few weeks of uncertainty over the supposed circular on mortgage caps, the UAE Central Bank recently issued further clarifications regarding the matter including the announcement of its plan to issue new regulations later in 2013.

Like most people that have a stake in the economy of the UAE, our initial concern was the impact it may have on property prices, rentals, the profitability of banks and financial institutions and the economy.

The clarifications are a positive step, not only because they have lifted the confusion surrounding the whole issue, but it has also sent a clear signal that the Central Bank will take whatever measures necessary to prevent property ‘gambling’ while at the same time indicating that it is willing to work with all concerned parties, especially the financial sector, on finding an appropriate solution.

The question, then, is, how do you prevent the ‘bubble-burst’ cycle from happening again, and should the Central Bank be the only player in this prevention?

In our opinion, there needs to be a more comprehensive solution that brings together both public and private institutions to achieve that goal. After all, banks and finance companies are a big part of the system. As much as they want to lend more money, they would also like to avoid losses such as those incurred at the end of 2008 and the costly legal actions that arise in such circumstances with little or no results.

Banks, which are a major part of the modern financial system, have great interconnections with the rest of the economy – unlike most other businesses. This makes the economy particularly vulnerable to shocks in the banking sector. Thus, banks have a duty of ensuring the greater good of an entire society and not simply making short-term profits.

We propose a number of remedies, by no means exhaustive, which may be considered in order to avoid a ‘bubble’ and maintain a healthy market.

1) First, banks must only be allowed to give loans to ‘qualified’ people or companies and only after conducting proper and comprehensive due diligence. There should be strict guidelines by the Central Bank with which banks must abide. Gone must be the days of unfettered loans and irresponsible lending valuation.

2) Second, the developers should not be allowed to sell off-plan properties until a minimum of at least 30 per cent construction of the project is complete. Of course, this would force developers to seek initial capital elsewhere, such as from banks, who have a much better ability to review projects, key personnel and the general viability and success of a construction project. In addition, this will also force a developer to reduce the number of simultaneous projects and, in case of a downturn or trouble with the developer, will mean a lesser shock to the system.

3) Another solution may include placing a ban or restriction in the form of high-transfer fees on the re-selling of ‘off-plan’ properties before the units are handed over. This would drive the ‘flippers’ and speculators out of the market while keeping the genuine buyers who are looking for a home to remain in the market since they are looking at long-term ownership rather than flipping of property.

4) Fourth, the Central Bank can place a ‘sliding scale’ on mortgage ratios based on the value of the property. The more expensive the unit, the bigger the percent down payment. This means that individuals will no longer be able to take large loans and buy beyond their means in order to play the market. This is something which happened extensively in the past and which exacerbated the financial shock.

5) Lastly, there needs to be improved policing of industry players such as brokers and evaluators and they should be made accountable for the statements they make. It is one thing if a taxi driver or a doctor makes comments about which way property prices are moving. However, it is a whole different matter when these ‘industry experts’ makes statements that are unsubstantiated or contradictory to the market reality. Simply saying ‘prices are set to increase’ or ‘current prices are about as high as pre-crisis levels’ should not be allowed or tolerated. These industry players must be held to a different standard than the rest of the population and when they make claims on price direction, they must back it with facts, otherwise they are simply ‘opinions’ that are being masqueraded as facts.

Will some or all of these proposals have a negative effect on certain people? Yes, nothing is without consequence and this will surely reduce some people’s ability to make a quick ‘dirham’. However, we need to look at the bigger picture and find ways in creating a more stable market so that in the long-term all can benefit from a responsible market place.

------------------------------

About the authors: Ahmad Waheed is an Associate in the Banking & Finance Department, and Victor Siriani is Marketing Manager at Bin Shabib & Associates LLP, a regional law firm

ALSO READ:

Horrific accident: Trailer truck smashes into back of bus killing 22 near Al Ain

Skycourts owners' call for dialogue over 'high' cooling charges

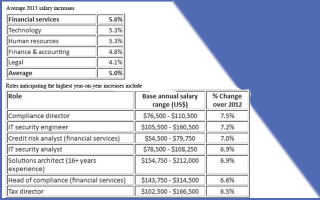

Salaries in UAE to rise 5% in 2013; finance professionals to see strongest gains

![]() Follow Emirates 24|7 on Google News.

Follow Emirates 24|7 on Google News.