- City Fajr Shuruq Duhr Asr Magrib Isha

- Dubai 04:25 05:43 12:19 15:46 18:50 20:09

(Shutterstock)

VAT is a tax levied by government on goods and services consumed by its people. So, VAT is a consumption tax.

As opposed to Sales Tax which is levied at the very last stage in the production and distribution chain, VAT is a multi-stage tax levied at each stage in the production and distribution chain and VAT is essentially levied on the value added at each stage. So, Sales Tax and VAT are different.

Each trader in the chain of supply from manufacturer through to retailer:

- Should collect VAT on their sales. (Output Tax)

- Can recover VAT paid on their purchases (Input Tax)

Practically, traders are entitled to deduct VAT on Purchases (Input Tax) from VAT on Sales (Output Tax) and the net liability is paid to the government (or a refund is claimed, in the case of negative liability).

The effect of offsetting VAT on purchases against VAT on sales is to impose the tax on the added value at each stage of production and distribution chain – hence Value Added Tax.

Such off-setting is generally allowed to traders quarterly on total basis by requiring them to file quarterly VAT Returns to the government.

For the final consumer, VAT simply forms part of the purchase price.

VAT is borne by the final consumer of goods or services while traders collect and account for the tax, in a way acting as a tax collector on behalf of the government.

At the end, government will receive through all the traders participated in the chain of production and distribution, an amount equal to the VAT paid by the final consumer.

How VAT woks?

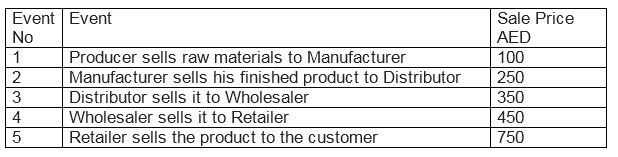

For explaining how VAT works, let us consider the below sequence of events in the chain of production and distribution.

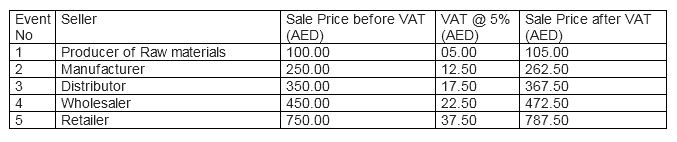

Assuming the VAT rate applicable to the product is 5%, the total price charged by each seller in the value chain shall be as follows:

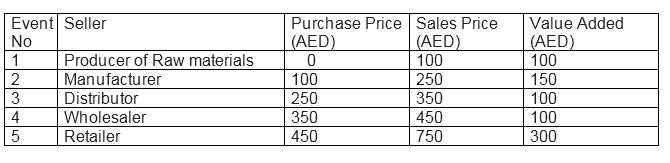

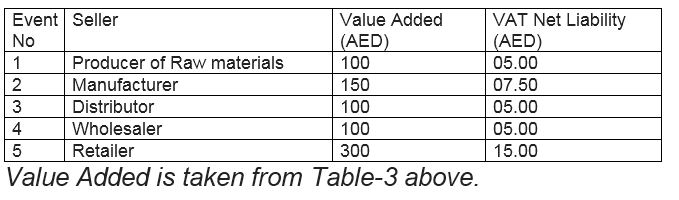

The value added by each Seller in the value chain are as follows:

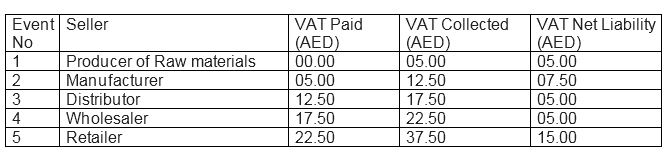

The VAT paid and collected by each Seller in the value chain are as follows:

VAT Net Liability of each seller is remitted by them to the Govt. periodically (generally quarterly) by filing VAT Returns.

All Sales, Purchases, VAT collected on Sales and VAT paid on Purchases of the Seller during a period (usually quarterly) are put together in the quarterly VAT return to arrive at the Net VAT Liability payable by the Seller or VAT Refund due to the Seller.

Analysis of the illustration for detailed understanding:

It can be observed that VAT Net Liability for each seller in the value chain is 5% VAT on the value added by him to the product.

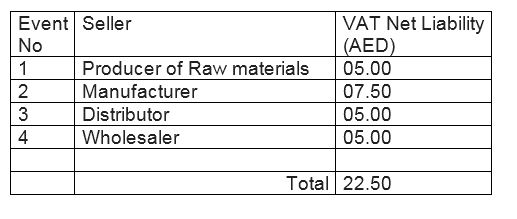

Please note that final Customer paid a VAT of Dh37.50 to the Retailer but the VAT remitted by the Retailer to the Government is only Dh15 because the balance Dh22.50 had already been paid by the sellers before him at various stages in the supply chain as below:

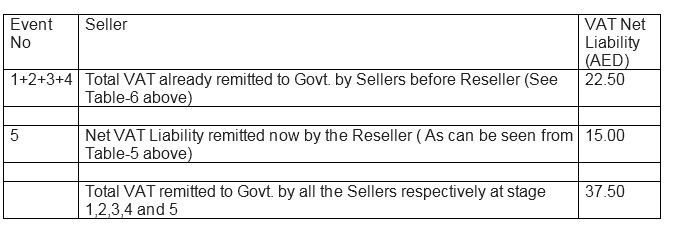

When the Retailer pays his VAT Net Liability, the total VAT collected by the Government on the product sold would be equal to the VAT paid by the final customer.

As you can observe, the above Dh37.50 is the VAT paid by the customer to the Reseller and the points to note are:

• Govt. does not wait for the sale to the final customer to happen to collect Dh37.50

• Rather, Govt. had already collected in advance a major portion of the Dh37.50 VAT now paid by the final customer to the Reseller.

• Govt. had collected this major portion of VAT from the sellers before the Reseller.

How the VAT of Dh37.50 paid by the final Customer to Reseller was collected by the Govt. sequentially from the various parties in the supply chain is shown below.

![]() Follow Emirates 24|7 on Google News.

Follow Emirates 24|7 on Google News.